January Rate Cut Off the Table

Week of January 13th, 2025

Welcome to AI8’s weekly newsletter, your ultimate source for curated insights and updates from the dynamic world of venture capital!

We’ve scoured the vast landscape of the web to bring you a comprehensive roundup of the industry’s top news articles, all in one convenient place. We keep you ahead of the game and in the know about all things related to the vibrant world of investments

STARTUPS

ROUNDS AND UNICORNS

The Week’s Biggest Funding Rounds: Data Storage And Lots Of Biotech (Crunchbase, 5 minute read)

DDN (Data Storage, $300M): Raised $300M from Blackstone Group, valuing the data storage company at $5B. DDN, founded in 1998, helps businesses manage and analyze data, particularly for AI models

Innovaccer (Healthcare, $275M): Raised $275M to enhance healthcare AI solutions. The San Francisco-based company, founded in 2014, provides software that improves patient experience and reduces administrative burden

Whatnot (E-commerce, $265M): Raised $265M in Series E at a $5B valuation. Whatnot, a livestream shopping platform, surpassed $3B in annual gross merchandise value in 2023

Aviceda Therapeutics (Biotech, $208M): Secured $207.5M in Series C funding. The biotech company, focused on immunomodulators for chronic inflammation, has raised $277M since its 2018 founding

Tenvie Therapeutics (Biotech, $200M): Raised $200M for neurological disease treatments. The South San Francisco-based biotech company was launched with support from Arch Venture Partners, F-Prime Capital, and Mubadala Capital

INDUSTRY

VC fund distributions will rebound in 2025 (Pitchbook, 3 minute read)

In 2025, venture fund distribution yields are expected to rebound for the first time since their peak in Q3 2021. After recent lows comparable to the global financial crisis (GFC), the decline in distributions is attributed to expedited market dynamics rather than systemic economic issues. Unlike the GFC, today’s environment features low unemployment, decelerating inflation, and robust public markets, setting the stage for recovery

Historical averages from 2010–2019 saw distribution yields at 16.4%, with a median of 9.2 years from founding to IPO

However, from 2020, low interest rates accelerated exits, shortening timelines and peaking distributions at 33% in Q3 2021

The resulting capital influx allowed funds to raise at record speed but left many overvalued companies behind when activity slowed

Increased pressure from LPs and improved exit conditions in 2025—buoyed by M&A-friendly policies and a strong pipeline of mature unicorns—are expected to reverse the distribution downtrend, reaching historical averages

VC fundraising in 2025 is projected to surpass 2024 levels, with capital raised estimated at $90 billion, up from $71 billion

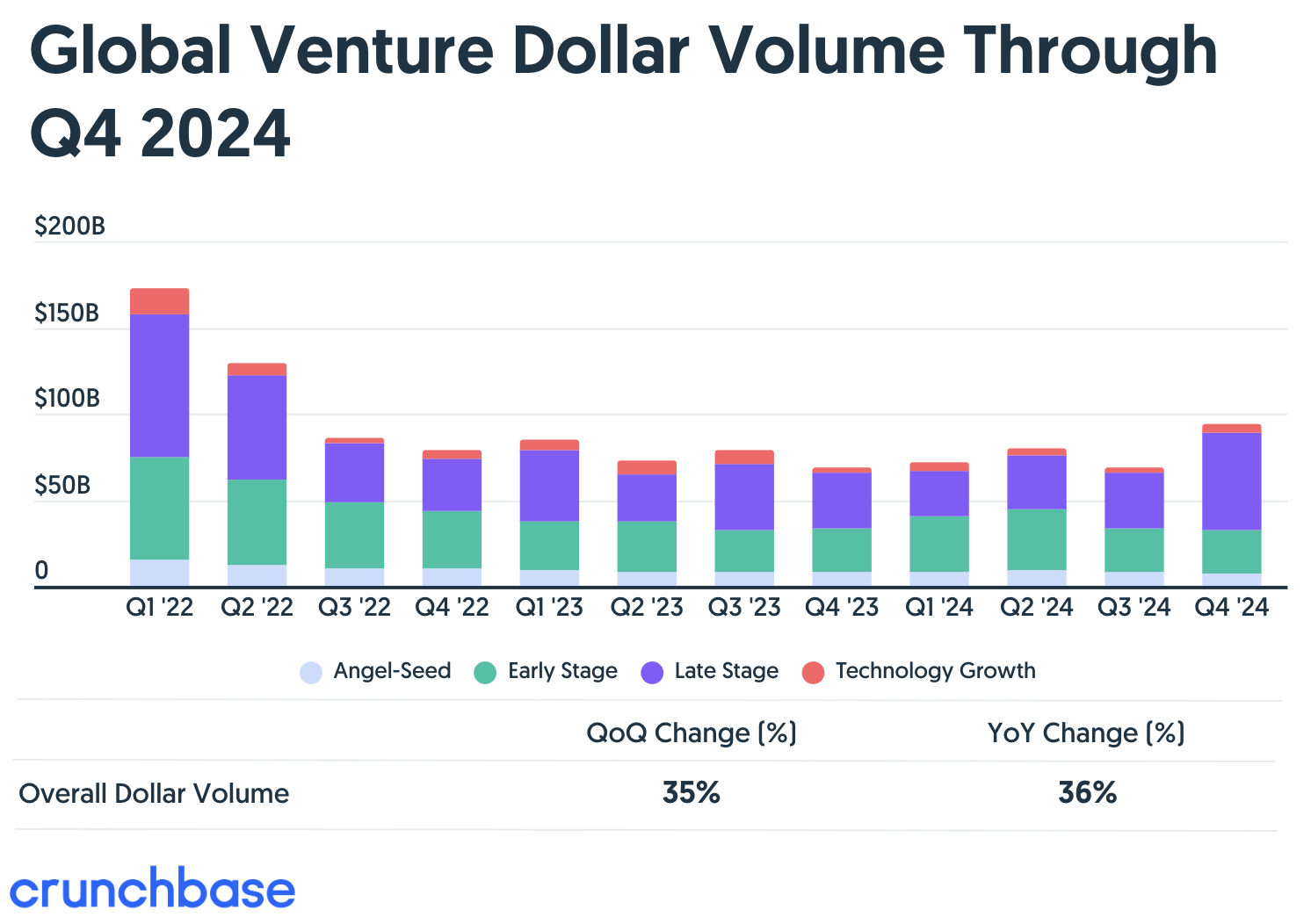

Startup Funding Regained Its Footing In 2024 As AI Became The Star Of The Show (Crunchbase, 5 minute read)

Global venture funding in 2024 reached $314 billion, a 3% increase from 2023, driven by a breakout year for AI, which attracted over $100 billion—80% more than in 2023. AI funding accounted for nearly a third of global venture investment, with significant contributions from foundation model companies and sectors like healthcare, robotics, and autonomous driving

The Q4 surge, totaling $93 billion, marked the highest funding since Q3 2022, fueled by billion-dollar rounds

Late-stage funding soared 70% QoQ to $61 billion, while early-stage funding remained flat, and seed funding declined slightly

US companies captured 57% of global funding, with $90 billion going to the Bay Area, largely due to AI investments

Liquidity remained tight, with M&A focused on biotech and cybersecurity, and the IPO market saw limited activity

AI startups grabbed a third of global VC dollars in 2024 (Pitchbook, 2 minute read)

In 2024, AI and ML startups captured 35.7% of global VC funding, with North America seeing nearly half of the total investment. This surge, totaling $131.5 billion, reflects growing interest in the sector, but some investors warn that the rush of capital is distorting the market. They argue that while there is substantial investment, it is often poorly allocated, with early-stage AI valuations disconnected from reality and overemphasizing foundational models and infrastructure

Some, like Samir Kumar of Touring Capital, expect corrections in 2025 as the market shifts

Others, like Shashank Saxena of Sierra Ventures, argue that the focus should move away from models like OpenAI and Anthropic and toward the application layer, where long-term returns will be realized

Despite the increased difficulty in identifying the best opportunities, investors like Casber Wang of Sapphire Ventures stress the importance of persistence in navigating this crowded space, acknowledging the increased potential payoff despite a higher "signal-to-noise" ratio

Silicon Valley is so dominant again, its startups devoured over half of all US VC funding in 2024 (Techcrunch, 2 minute read)

Despite discussions about San Francisco's decline, the Bay Area remains the premier hub for venture-backed startups. In 2024, Bay Area startups secured $90 billion of VC funding, accounting for 57% of the $178 billion in U.S. venture funding, according to Crunchbase. Notable players include OpenAI, which has driven the local AI ecosystem, Databricks with a record-breaking $10 billion funding round, and xAI raising $12 billion, among others

The region's dominance is fueled by its concentration of Big Tech companies (Google, Nvidia, Salesforce), robust startup infrastructure (Y Combinator, Sand Hill Road), and a skilled talent pool

Nearly half of all Big Tech engineers and 27% of startup engineers are based in the Bay Area, providing founders with access to talent, customers, and investors

The region's density of resources creates a self-reinforcing cycle, which shows no signs of slowing in 2025

INDUSTRY INTERNATIONAL

Latin America Startup Funding Ticked Higher In 2024 (Crunchbase, 5 minute read)

Latin American startup investment reached $4.2 billion in 2024, a 27% increase from 2023, driven by late-stage funding gains in Q4, which marked the year’s highest quarterly total. However, funding remains well below 2021 and early 2022 peaks. Fintech dominated the region’s funding, highlighted by major rounds like Ualá's $300M Series E and Asaas’s $133M Series C

Brazil led with nearly half the total investment, followed by Mexico, which captured one-fifth

Digital commerce also saw strong funding, with companies like Mexico-based Clip and OCN raising significant rounds

While IPOs and acquisitions were sparse in 2024, a robust pipeline of mature startups suggests potential for increased exit activity in 2025, especially if IPO markets rebound

VC investment in emerging markets plummeted by over 40% last year (Techcrunch, 2 minute read)

Venture capital investment in emerging markets like the Middle East and North Africa (MENA), Africa, Southeast Asia, Türkiye, and Pakistan dropped 41% in 2024 to $9.1 billion, with deal activity down 20%, reflecting global VC funding declines outside AI sectors. The MENA region experienced a smaller funding drop of 29% ($1.9 billion) compared to Southeast Asia (45%) and Africa (44%)

Fintech remained strong, securing $3.9 billion across all regions

Despite reduced late-stage capital and a 32% global dip in exits, MENA saw a 7% increase in deal count and an 18% rise in investors

International investors focused on late-stage deals, while local investors prioritized early-stage funding

ECONOMIC SNAPSHOT

U.S. labor market ends 2024 with a bang, adding 256,000 jobs (Axios, 4 minute read)

The U.S. economy added 256,000 jobs in December 2024, significantly surpassing expectations of 155,000 and bringing the unemployment rate down to 4.1%, signaling continued labor market resilience. This strong job growth caps a year of robust hiring, defying economic concerns and supporting prospects of a soft landing for the economy

Federal Reserve officials are closely monitoring these figures, which may justify holding interest rates steady as inflation progress remains stalled

While layoffs have been minimal, uncertainties persist, with concerns over potential inflationary pressures from aggressive trade and deportation policies under President-elect Trump

Revisions showed November's job gains were slightly lower at 212,000, while October saw a modest upward revision to 43,000

Strong December Jobs Report Kills Chances Of A January Fed Rate Cut (Forbes, 7 minute read)

The December 2024 jobs report highlighted a robust labor market with the unemployment rate dropping to 4.1% from 4.2% exceeding expectations and reducing recession fears but also significantly lowered the likelihood of a Federal Reserve interest rate cut on January 29, with probabilities falling to just 2.7%. Elevated inflation remains a concern, with November year-on-year rates for total CPI at 2.7% and core CPI at 3.3%, while total PCE and core PCE inflation were at 2.4% and 2.8%, respectively

Inflation is expected to ease toward the Fed's 2% target by late 2025, but this delay suggests the next rate cut, a potential 0.25% reduction, may not occur until May 2025

Markets reacted to the report with bond yields and the dollar strengthening, while equities, bond prices, and industrial commodities faced pressure

The upcoming December CPI report on January 15 may further influence inflation expectations and Fed policy, as the central bank maintains a cautious stance in light of slowing labor market growth

'Trump 2.0' looms large over the global economy (BBC, 6 minute read)

The global economy in 2025 is projected to grow at a modest 3.2%, with inflation, interest rates, and trade tensions posing significant challenges. Central banks are struggling to bring inflation down to target levels, with rates in the US (2.7%), eurozone (2.2%), and UK (2.6%) remaining elevated. The US Federal Reserve has signaled caution on further interest rate cuts, while persistent wage pressures worldwide contribute to inflationary risks

Trade tensions are intensifying as Donald Trump’s return to the presidency brings threats of new tariffs on key trading partners like China, Canada, and Mexico

In China, growth is forecast to improve to 4.5% despite domestic challenges, but trade tensions remain a key risk. Meanwhile, the eurozone faces slowing momentum amid political instability and stubborn inflation

Globally, the jobs market reflects a lack of economic dynamism, with businesses passing rising costs onto consumers, further fueling inflation

IMPACT & CLIMATE RESILIENCE

How could Trump’s second term affect DEI initiatives in the US? (The Guardian, 5 minute read)

Several major companies, including Walmart, McDonald’s, and Meta, have recently scaled back or eliminated their Diversity, Equity, and Inclusion (DEI) programs, with Meta citing changes in the legal and policy landscape as a key factor. While some actions stemmed from conservative social media pressure, others appeared unprompted, reflecting a broader shift away from post-2020 commitments to diversity

Trump-appointed judges and a conservative Supreme Court are shaping legal interpretations, making companies wary of reverse discrimination lawsuits

Since the 2023 Supreme Court ruling against affirmative action in education, many private employers have quietly rolled back their DEI programs to avoid potential legal and political fallout

Despite these challenges, DEI advocates emphasize the importance of maintaining initiatives within legal bounds, fostering inclusivity internally, and publicly defending the value of diversity

Meta Latest To Dump DEI: Here Are The Companies Ending Diversity Programs (Full List) (Forbes, 6 minute read)

Meta announced the end of several diversity, equity, and inclusion (DEI) programs, citing changes in the U.S. legal and policy landscape as a driving factor, making it the latest in a series of corporations to scale back DEI initiatives amid growing conservative backlash. Since 2020, when DEI policies gained momentum following anti-racism protests, companies such as McDonald’s, Walmart, Boeing, and John Deere have rolled back DEI commitments

Reasons include the 2023 Supreme Court ruling against affirmative action and pressure from conservative activists

Critics argue that these moves are responses to legal and political challenges, as well as public campaigns by figures like Robby Starbuck, who actively targets "woke" policies

While some companies retreat, others like Costco continue to defend DEI as vital for fostering inclusivity and driving innovation

IPO & EXITS

Forecast: 13 Companies That Could Go Public In 2025 If The IPO Market Gains Steam (Crunchbase, 6 minute read)

The IPO market, after three years of stagnation, could see renewed activity in 2025 despite 2024’s lackluster performance. While many large private companies have relied on significant capital reserves, the need for venture-backed startups to eventually exit through acquisitions or public offerings remains inevitable. Crunchbase News highlights 13 contenders poised for potential IPOs

In enterprise tech and AI, Cerebras Systems, CoreWeave, Snyk, and SymphonyAI stand out, with strong financials and strategic moves

The fintech sector could see entries from Stripe, Klarna, and Revolut, each demonstrating robust growth and market readiness

In health and biotech, Hinge Health and Element Biosciences are preparing for potential IPOs, leveraging their respective advancements in virtual physical therapy and genetic analysis tools

Consumer-focused companies like Navan, StubHub, and Discord also seem primed for market debuts, along with design-software maker Canva

Forecast Digest: IPO, M&A And Venture Markets Expected To Gain In 2025 (Crunchbase, 3 minute read)

The startup ecosystem starts 2025 on a positive note, with renewed optimism fueled by a rebound in venture funding, a recovering IPO market, and expectations of increased M&A activity. The IPO market, sluggish in 2024, is anticipated to gain momentum, with tech sectors like fintech, AI, and cybersecurity leading the way. Key exits like ServiceTitan’s IPO highlight the potential for more large-scale debuts, unlocking unrealized value in late-stage startups

M&A activity is also expected to rise, driven by leadership changes at regulatory agencies and a more business-friendly U.S. administration, which could encourage acquisitions stalled under stricter regulations

AI remains a dominant force, capturing nearly one-third of all global venture capital in 2024 and breaking investment records

Despite the optimism, challenges remain: proposed tariffs and inflationary pressures could impact interest rates, while uncertainty around immigration policies and antitrust enforcement could affect talent and big tech

AI8 VENTURES HIGHLIGHT

Trumponomics 2.0

Following President-elect Donald J. Trump’s victory over Kamala Harris, the financial world witnessed an immediate response. In just one week, the S&P 500’s value surged by $1.9 trillion, pushing stocks to record highs. The U.S. dollar strengthened globally and Bitcoin achieved unprecedented highs.

Wall Street is preparing for more government spending, lighter regulation, bigger deficits, and accelerating growth under a Trump administration and a Republican-led Congress.

Biden’s Economic Legacy

The Biden era was marked by headlines of massive layoffs and a cost of living crisis. The average worker faced double-digit increases in food, energy, housing, and other essential expenses that impacted middle-class families the most and consumed the bulk of household budgets. Despite record highs in the stock market, nearly half of Americans believed the nation was in a recession. Is this Biden’s fault? No. Global supply chain disruptions, stimulus checks, the aftermath of COVID-19 lockdowns, and the ripple effects of geopolitical tensions all contributed to soaring prices. Did Americans blame Biden? Election results suggest they did. Two-thirds of voters believed the economy was on the wrong track.

Hence, Trumponomics 2.0.

Trump’s campaign capitalized on promises of economic revival, pledging to deliver low taxes, low regulations, low energy costs, low interest rates, and low inflation -Trumponomics.

Alpha Insights on Trump and AI in Mexico City

Last week, we hosted our first Alpha Insights event in Mexico City, where we brought together industry experts, investors, and entrepreneurs to discuss the evolving landscape under the new U.S. administration. We dove into how the election of Donald Trump, "Trumponomics," and the transformative role of AI are shaping the future of investments, regulations, markets, taxes, and cross-border opportunities.

Missed the event? We’ve curated the key insights in our Alpha Insights Special Edition: Trumponomics Report. Understand everything VC-related that happened in 2024 and how profit will shift under Trump 2.0

(Trumponomics 2.0 Special Edition starts on page 22)

Alpha Insights: 2024 Venture Capital Report

Alpha Impact 8 Ventures is thrilled to share our latest insights into the dynamic world of investments with our 2024 Venture Capital Report.

Last year, Michael Burry, the legendary fund manager who famously profited from shorting the US housing market in 2008, bet more than $1.6 billion on a Wall Street crash by shorting the S&P 500 and Nasdaq-100. Nothing happened.

This year, Warren Buffett’s cash reserves reached a record $276.9 billion as Berkshire Hathaway trimmed its stock holdings in Apple. Some view it as a routine adjustment, while others speculate that Buffett perceives an overheated, overvalued market.

Everyone talks about a soft landing, but warning signs are flashing and the world seems to be teetering on a delicate balance. Is there something we’re missing? Is there an unseen factor at play?

Alpha Impact 8 Ventures is disrupting the industry, generating wealth, creating technology, providing access, leveling the play field, reducing systemic barriers, and building a resilient world.

Become part of the our revolution.

Happy reading,

AI8 Ventures’ Research & Investment Team