2025: The Year of IPO Revival?

Week of December 30th, 2024

Welcome to AI8’s weekly newsletter, your ultimate source for curated insights and updates from the dynamic world of venture capital!

We’ve scoured the vast landscape of the web to bring you a comprehensive roundup of the industry’s top news articles, all in one convenient place. We keep you ahead of the game and in the know about all things related to the vibrant world of investments

STARTUPS

ROUNDS AND UNICORNS

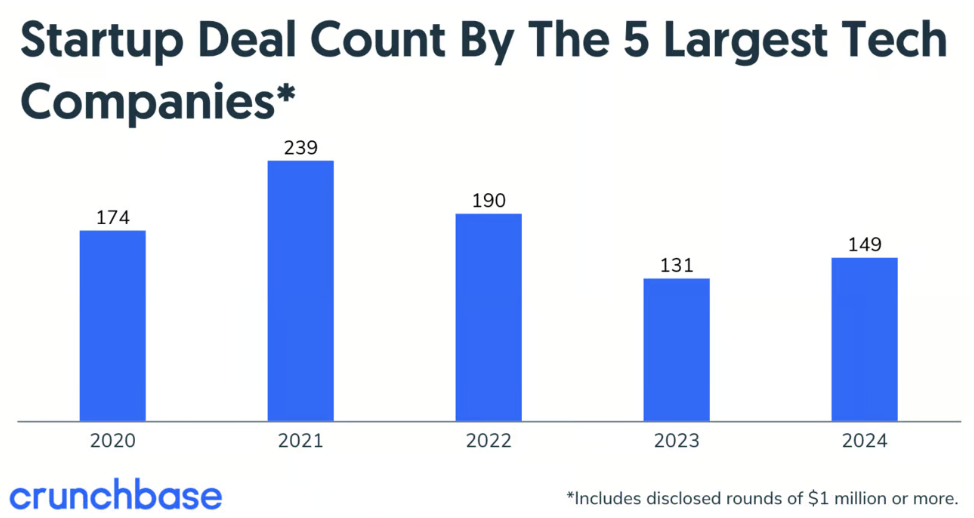

The Big 5 Didn’t Binge On Startup Investments In 2024 (Crunchbase, 5 minute read)

In 2024, the five most valuable tech companies—Apple, Microsoft, Nvidia, Amazon, and Alphabet—had ample funds for startup investments, but they were not highly active in venture deals. Collectively, they invested in 149 known startup financings of $1 million or more, marking the second-lowest total in the past five years. Despite this, they participated in some large funding rounds, primarily for AI companies

The biggest was OpenAI's $6.6 billion round, followed by Alphabet’s $5.6 billion investment in Waymo and Amazon’s $4 billion funding of Anthropic

Alphabet was the most active investor, leading 87 rounds, while Apple was the least active, with no disclosed rounds

With strong cash reserves, high stock prices, and ongoing pressure to lead in AI, these companies are well-positioned for further investments

Europe Vs. Silicon Valley 2025: Can Europe Dominate The Unicorn Race? (Forbes, 6 minute read)

Silicon Valley (SV) remains the dominant force in unicorn development, but emerging venture hubs like Shenzhen, Beijing, Singapore, Tel Aviv, and Europe, particularly the 5-hour radius around London, are positioning themselves as challengers. SV’s success is rooted in three key factors: leadership in emerging industries, a dense ecosystem of entrepreneurial talent and angels where 1 in 100,000 ventures becomes a unicorn, and the ability to attract the world’s best entrepreneurs

In contrast, Europe’s unicorn development often mirrors existing SV successes rather than pioneering new industries, and it faces challenges in attracting and retaining top entrepreneurial talent and bold investors

To compete, Europe must build its own Unicorn-Entrepreneur Ecosystem by empowering diverse entrepreneurs to act independently of venture capital and fostering innovation in emerging industries

INDUSTRY

Nearly 1 in 4 new startups is an AI company (Pitchbook, 5 minute read)

AI startups now represent 22% of first-time VC financings, with $7 billion raised in AI and machine learning companies in 2024, according to PitchBook data. This marks a historic high for the sector, which has outpaced others in valuation and unicorn creation. However, investors are increasingly concerned about "AI washing," where companies claim to be AI-driven without offering true innovation

As AI costs drop, it has become almost necessary for many startups to integrate AI to attract funding

Brendan Burke of PitchBook notes that development costs are falling, and even non-AI companies must incorporate generative AI to secure investment

Despite this, some investors advocate for continued expansion in the sector, believing the opportunities in AI are vast and should be encouraged, even without focusing on efficiency or limitations

Industry spotlight: Fintech fundraising is trending up in 2024 (Carta, 5 minute read)

In the first nine months of 2024, fintech startups on Carta raised approximately $3.8 billion in venture capital, nearly matching the total raised in all of 2023. This marks a recovery after the sharp fundraising slowdown in 2023. Despite this bounceback, investor caution remains evident, with fintech deal counts steady at around 110 per quarter, but seed-stage activity slowing down, with fewer than 40 deals in Q2 and Q3

Additionally, 20% of fintech investments have been down rounds in four of the past five quarters, highlighting a more cautious investment approach

Bridge rounds have become common, with nearly 50% of seed and Series A deals in Q3 being bridge rounds as companies seek interim funding

Seed valuations and deal sizes have fluctuated, with seed valuations dropping by 21% from Q1 2024, and median seed deal sizes shrinking in recent quarters

Poor Valuation Practices Have Slowed Innovation (Crunchbase, 5 minute read)

Professional investing hinges on understanding value and how it appreciates over time. Historically, venture capital firms that could recognize value in emerging sectors—such as online marketplaces in 1997, space in 2002, or crypto in 2012—earned outsized returns. However, the software investment boom over the past decade has shifted the focus of venture capital to SaaS-style growth metrics like ARR multiples, overshadowing fundamentally innovative ideas

This shift has created a "virtuous loop" where VCs prioritize rapid capital deployment for scalable SaaS businesses, leading to the rise of mega funds

The use of crude ARR multiples as a default valuation method has undermined discipline in deal-making, especially for deep tech startups that require longer R&D periods and lack immediate revenue growth

This environment has fostered a short-term trader mentality, making venture capital more focused on quick gains rather than long-term, sustainable value

ECONOMIC SNAPSHOT

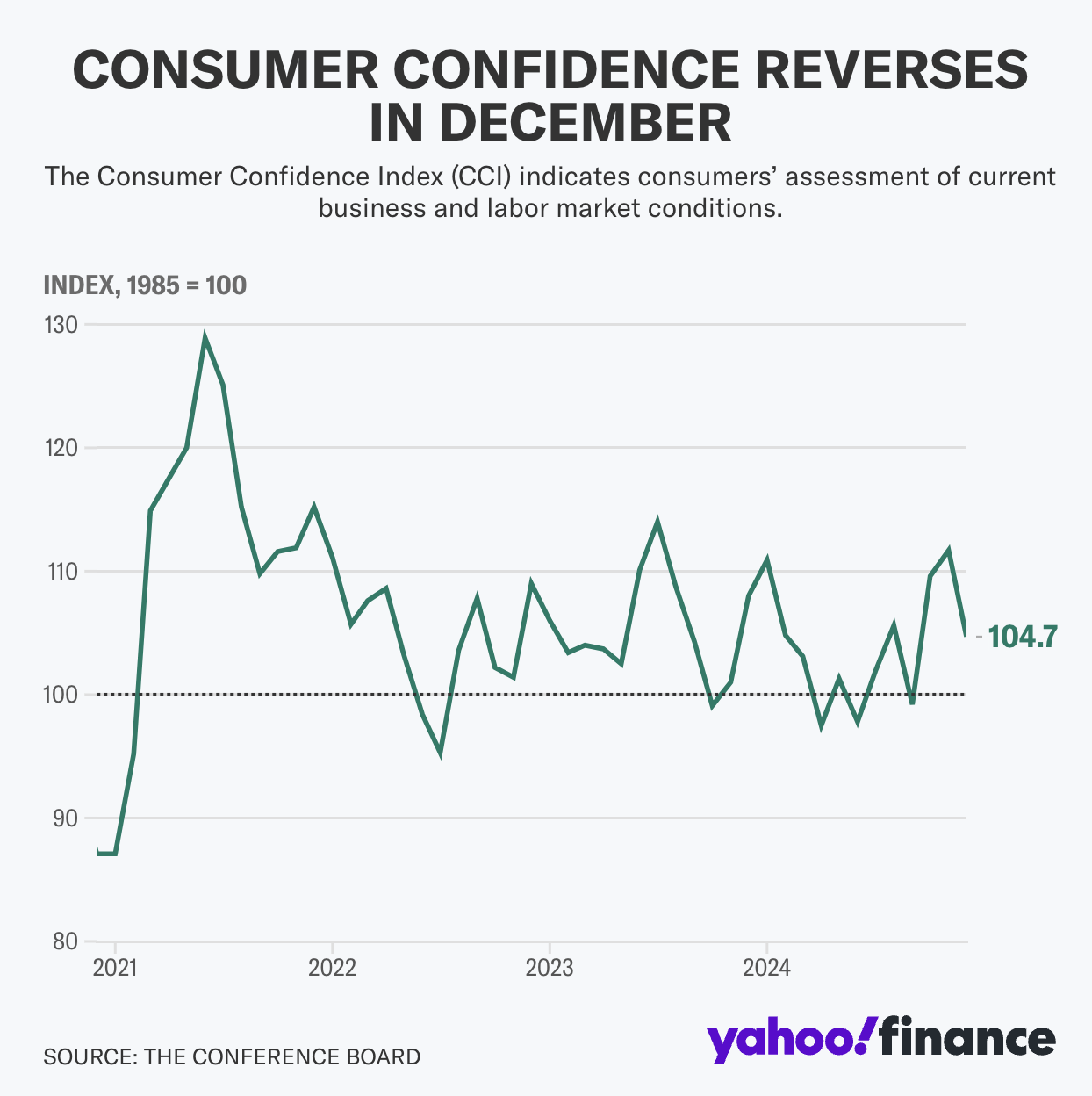

Americans are less confident about where the US economy is headed (Yahoo Finance, 4 minute read)

US consumer confidence dropped sharply in December, with the Conference Board's consumer confidence index falling by 8.1 points to 104.7, below the expected 113.2. The expectations index, which reflects views on income, business, and labor market conditions, plunged 12.6 points to 81.1, signaling potential recession risks

Consumers were notably less optimistic about future business conditions and incomes, and pessimism about job prospects returned

The rise in concerns about tariffs and political policies also contributed to the decline

The percentage of consumers expecting fewer jobs increased to 21.3%, and fewer expected higher stock prices in the next year

2025 Outlook: 5 Trends That Will Impact The Economy And Markets (Forbes, 6 minute read)

The U.S. economy is expected to experience positive trends in 2025, despite some challenges. Here are key factors shaping the outlook:

Labor Market: The U.S. labor market remains strong with low unemployment (4.2% in November 2024) and more than 7.7 million job openings in October 2024. Payroll growth may slow in 2025, but significant job losses are unlikely, supporting a stable job market

Consumption: Solid consumer spending, driven by a strong job market and rising wages, is expected to continue in 2025. Retail sales and personal consumption expenditures have been robust, and consumer debt delinquencies remain low

Growth: U.S. GDP growth is forecasted to decelerate in 2025 after strong performance in 2024. However, consumption will remain a key growth driver, supported by low consumer debt delinquencies and strong job gains

Inflation: Inflationary pressures are expected to ease in 2025, with consumer inflation rates likely falling due to base effects and modest month-on-month inflation in recent reports. While inflation is still above the Fed’s 2% target, it is projected to decrease gradually

Interest Rates: Following the Fed's rate cuts in 2024, further rate cuts are expected in 2025, with projections for at least two 0.25% cuts

The Fed Is Unlikely To Cut Interest Rates In January Due To Inflation (Forbes, 4 minute read)

The Fed cut interest rates by 0.25% on December 18, 2024, lowering the federal funds rate to a range of 4.25%-4.50%. However, another rate cut at the January 29, 2025, meeting is highly unlikely, with a 92.5% chance of no change according to the CME FedWatch Tool. Elevated U.S. consumer inflation—November year-on-year rates include total CPI at 2.7% and core CPI at 3.3%—along with low unemployment, reduce urgency for further cuts

The December FOMC projections suggest only two 0.25% rate cuts in 2025, compared to four cuts projected in September

Despite this, some experts, such as Prestige Economics, anticipate at least three rate cuts in 2025, with the next one likely by May

Inflation, particularly core CPI, remains a concern as December CPI is expected to rise closer to 3%, potentially delaying Fed action

What's the Outlook for Interest Rates in 2025? (Investopedia, 5 minute read)

The Fed has scaled back its projections for interest rate cuts in 2025, which could keep borrowing costs high across various loan types. Mortgage rates are expected to remain elevated, with forecasts suggesting they will stay above 6%, influenced more by 10-year Treasury yields than the Fed’s rate decisions. However, economists predict mortgage and auto loan rates may rebound after an initial drop in early 2025

Credit card interest rates, now averaging 24.37%, could see some relief as prior Fed rate cuts take effect, but borrowers should stay vigilant, as credit card APRs are variable and subject to change

Uncertainty looms over the broader economic landscape, with potential tariffs from President-elect Donald Trump posing a risk of increased inflation

If price pressures rise, the Federal Reserve may need to slow or halt additional rate cuts

IMPACT & CLIMATE RESILIENCE

Businesses owned by people of color and women pay significantly higher loan interest rates, study finds (Marketplace, 3 minute read)

The Federal Reserve's interest rate policies significantly impact borrowing costs for individuals and businesses, yet lenders have considerable discretion in determining rates, often leading to disparities. A University of Washington study found businesses owned by women and people of color face markedly higher interest rates, costing an additional $8 billion annually

Black-owned businesses pay up to 3% more in interest than white-owned businesses, with Hispanic-owned businesses paying 2.9% more

Minority-owned businesses are also more likely to face higher collateral requirements and be denied trust from lenders

Such inequities force minority-owned businesses into less capital-intensive industries, limiting their potential for job creation and broader economic growth

DEI programs weathered a myriad of attacks this year, with more to come in 2025 (NBC News, 6 minute read)

In 2024, DEI programs faced significant setbacks, with major companies like Walmart and Ford scaling back amid rising opposition from figures like Elon Musk and influencers like Robby Starbuck. States such as Utah and Iowa joined others in banning DEI offices or requirements in universities, while President-elect Trump pledged to end federally funded DEI initiatives. Critics argue these programs lower standards, while advocates highlight their role in equity and innovation

Despite the backlash, some leaders, like JPMorgan’s Jamie Dimon and Mark Cuban, continue supporting DEI, citing its business benefits

Surveys show student support for DEI remains strong, with over 50% of Republican students viewing it positively

Advocates stress that rebranding and individual action are key to sustaining DEI's progress

IPO & EXITS

IPOs Gained Momentum in 2024. Next Year Could Be Even Bigger (Investopedia, 4 minute read)

The U.S. IPO market had its strongest year since 2021, with companies raising over $41 billion in 2024, up from $24 billion in 2023 and $22 billion in 2022. While this remains a fraction of the record $316.6 billion raised in 2021, investor optimism for 2025 is high, fueled by recent interest-rate cuts and pro-business policies anticipated under the Trump administration, including deregulation and potential tax reforms

Key IPOs anticipated for next year include Cerebras Systems and Klarna, which could set the tone for others, such as crypto-related firms, to follow suit if these listings perform well

However, robust private markets, as seen with companies like SpaceX and OpenAI, continue to provide strong alternatives to public funding

In 2024, Lineage led the year’s IPO activity with a $5.10 billion raise, followed by Viking Holdings ($1.77 billion), StandardAero ($1.66 billion), Amer Sports ($1.57 billion), and UL Solutions ($1.09 billion)

Why IPOs Are Losing Their Luster In A Changing Economy (Forbes, 5 minute read)

The news of Chime filing for a potential 2025 IPO has sparked optimism about a revival in public listings, especially following ServiceTitan’s recent debut. Speculation surrounds other major players like Klarna, StubHub, Stripe, and Revolut potentially joining the fray. However, expectations for a broad IPO resurgence may be overly optimistic. Historical caution remains, with past examples like Groupon and Zynga illustrating the risks of post-IPO underperformance—Groupon’s valuation plummeted by 99% since its IPO, while Zynga’s share price dropped 70% within a year of its 2011 debut

Market volatility, high interest rates, and economic uncertainties further deter many late-stage startups from going public

Despite high valuations, many companies still grapple with profitability due to prior growth-focused strategies, with Amazon itself taking nearly seven years post-IPO to achieve its first profit

The private markets, meanwhile, have undergone a fundamental shift, offering alternatives like secondary marketplaces and employee stock options for liquidity

2025 is likely to see a cautious, selective IPO landscape where strategy and timing take precedence over volume

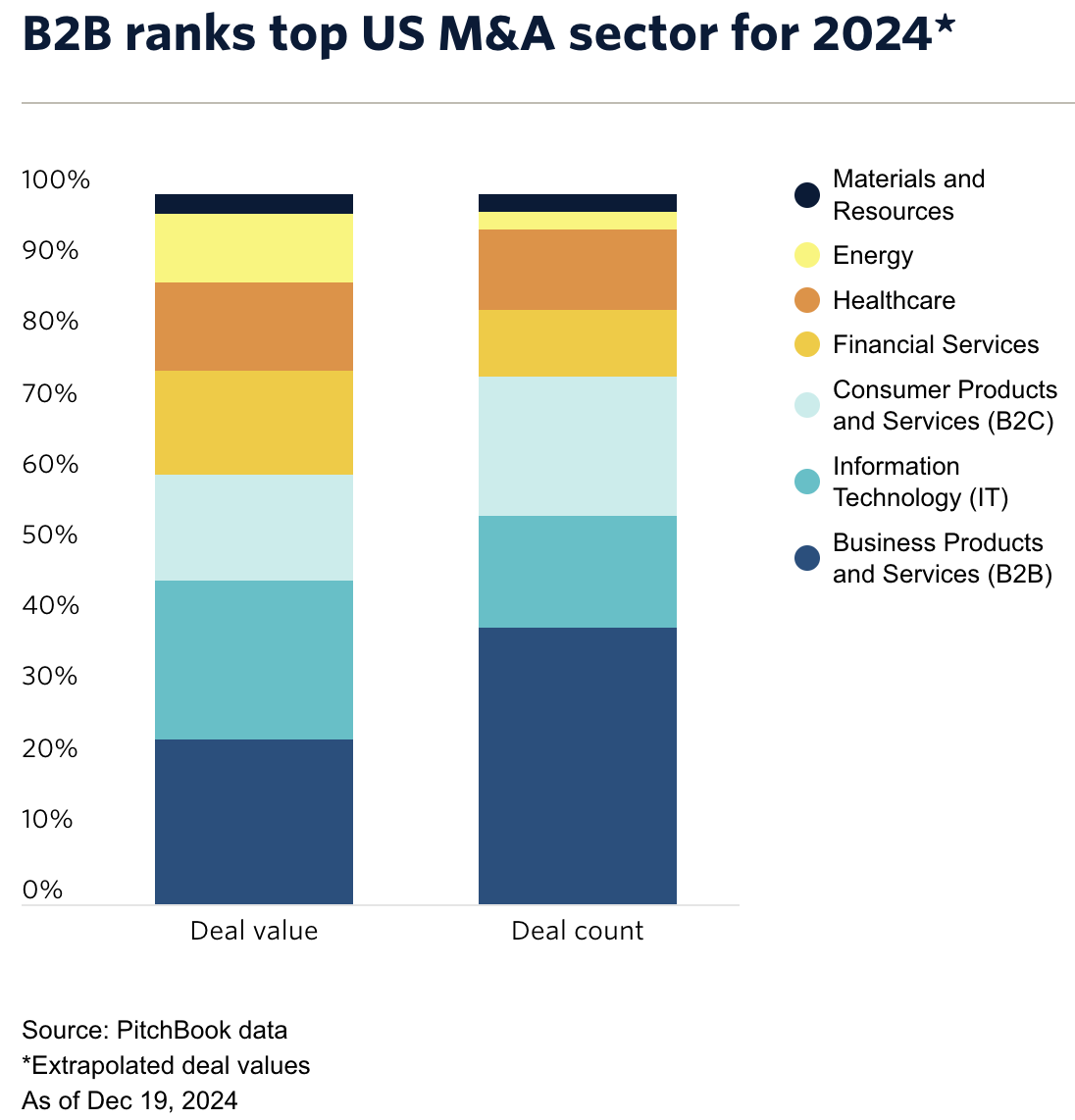

M&A 2024: Rebounding from rates and regulations (Pitchbook, 4 minute read)

In 2024, the venture capital landscape showed signs of recovery but faced ongoing challenges, particularly around regulatory scrutiny. Early in the year, corporate buyers were more active than private equity due to high borrowing costs and a sluggish exit environment. However, by Q3 2024, VC-backed deal activity rebounded as interest rates began to lower

Despite the recovery, the impact of the FTC’s intensified scrutiny, particularly under Lina Khan’s leadership, created significant uncertainty for venture investors

Corporate cash reserves remain steady, while PE dry powder is trending downward, giving corporate buyers an advantage

The largest deal of 2024 was Mars acquiring Kellanova, valued at $36 billion in the consumer products and services sector

AI8 VENTURES HIGHLIGHT

Trumponomics 2.0

Following President-elect Donald J. Trump’s victory over Kamala Harris, the financial world witnessed an immediate response. In just one week, the S&P 500’s value surged by $1.9 trillion, pushing stocks to record highs. The U.S. dollar strengthened globally and Bitcoin achieved unprecedented highs.

Wall Street is preparing for more government spending, lighter regulation, bigger deficits, and accelerating growth under a Trump administration and a Republican-led Congress.

Biden’s Economic Legacy

The Biden era was marked by headlines of massive layoffs and a cost of living crisis. The average worker faced double-digit increases in food, energy, housing, and other essential expenses that impacted middle-class families the most and consumed the bulk of household budgets. Despite record highs in the stock market, nearly half of Americans believed the nation was in a recession. Is this Biden’s fault? No. Global supply chain disruptions, stimulus checks, the aftermath of COVID-19 lockdowns, and the ripple effects of geopolitical tensions all contributed to soaring prices. Did Americans blame Biden? Election results suggest they did. Two-thirds of voters believed the economy was on the wrong track.

Hence, Trumponomics 2.0.

Trump’s campaign capitalized on promises of economic revival, pledging to deliver low taxes, low regulations, low energy costs, low interest rates, and low inflation -Trumponomics.

Alpha Insights on Trump and AI in Mexico City

Last week, we hosted our first Alpha Insights event in Mexico City, where we brought together industry experts, investors, and entrepreneurs to discuss the evolving landscape under the new U.S. administration. We dove into how the election of Donald Trump, "Trumponomics," and the transformative role of AI are shaping the future of investments, regulations, markets, taxes, and cross-border opportunities.

Missed the event? We’ve curated the key insights in our Alpha Insights Special Edition: Trumponomics Report. Understand everything VC-related that happened in 2024 and how profit will shift under Trump 2.0

(Trumponomics 2.0 Special Edition starts on page 22)

Alpha Insights: 2024 Venture Capital Report

Alpha Impact 8 Ventures is thrilled to share our latest insights into the dynamic world of investments with our 2024 Venture Capital Report.

Last year, Michael Burry, the legendary fund manager who famously profited from shorting the US housing market in 2008, bet more than $1.6 billion on a Wall Street crash by shorting the S&P 500 and Nasdaq-100. Nothing happened.

This year, Warren Buffett’s cash reserves reached a record $276.9 billion as Berkshire Hathaway trimmed its stock holdings in Apple. Some view it as a routine adjustment, while others speculate that Buffett perceives an overheated, overvalued market.

Everyone talks about a soft landing, but warning signs are flashing and the world seems to be teetering on a delicate balance. Is there something we’re missing? Is there an unseen factor at play?

Alpha Impact 8 Ventures is disrupting the industry, generating wealth, creating technology, providing access, leveling the play field, reducing systemic barriers, and building a resilient world.

Become part of the our revolution.

Happy reading,

AI8 Ventures’ Research & Investment Team